State Farm Wildfire Insurance Withdrawal Guide for 2026

The 2026 state farm wildfire insurance withdrawal is creating uncertainty for thousands of Los Angeles homeowners. As insurers retreat from wildfire-prone regions, many families are left questioning how to protect their homes and investments.

In this guide, we break down the reasons behind the state farm wildfire insurance withdrawal, what it means for your coverage, and the immediate actions you should take. You will learn about practical steps to secure replacement insurance, proven wildfire defense strategies, and how partnering with Matador Fire can help you safeguard your property and improve your insurability.

Let’s explore your options and restore your peace of mind.

Understanding the State Farm Wildfire Insurance Withdrawal in 2026

In 2026, State Farm’s decision to stop renewing and writing new home insurance policies in wildfire-prone areas has sent shockwaves through our community. This move is not just a headline — it is a sign of deeper changes in how insurers view wildfire risk across California.

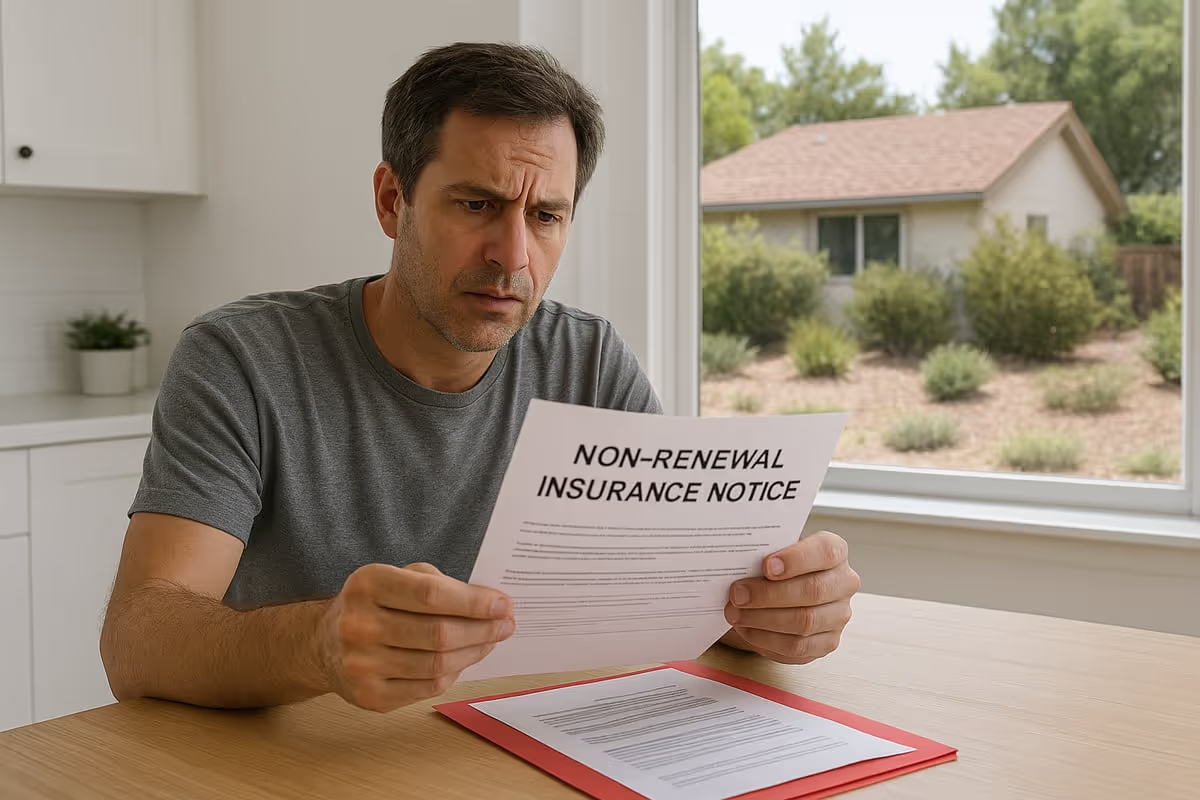

What exactly does the state farm wildfire insurance withdrawal mean for homeowners? Starting in 2026, State Farm will no longer offer or renew standard home insurance policies for thousands of properties located in areas identified as high wildfire risk. This process began in earnest in 2024, when State Farm canceled or declined to renew more than 72,000 home and apartment insurance policies in California, a decision that affected many residents in the hills and canyons of Los Angeles. For more on the initial impact, see State Farm's 2024 policy cancellations.

Why are insurers, including State Farm, taking this drastic action? There are several factors at play. First, California has experienced a dramatic rise in wildfire losses over the past decade. The cost of claims from catastrophic fires has far outpaced premium income, putting immense financial pressure on carriers. Second, advances in risk modeling now allow insurers to pinpoint properties with higher wildfire exposure, leading to more selective underwriting and more frequent non-renewals.

Regulatory pressures also play a major role in the state farm wildfire insurance withdrawal. California’s insurance laws limit how much insurers can raise rates, even as wildfire risks increase. This has created a situation where companies like State Farm feel they can no longer balance risk and reward, prompting them to exit the market rather than face ongoing losses.

The impact of the state farm wildfire insurance withdrawal is especially acute in Los Angeles and surrounding counties. In 2024 alone, over 30,000 policies were non-renewed in the region, leaving homeowners scrambling to find alternative coverage. Areas such as Malibu, Topanga, and the foothills of Pasadena are among the hardest hit, as their combination of dense vegetation, steep terrain, and history of major wildfires make them less attractive to traditional insurers.

This withdrawal is not an isolated event. It is part of a broader trend across wildfire-prone states, where major carriers are reducing their exposure to high-risk properties. As more insurers follow State Farm’s lead, homeowners face shrinking options, higher premiums, and stricter requirements for coverage. The California Department of Insurance has acknowledged the crisis, issuing statements and seeking solutions to stabilize the market and protect consumers.

For homeowners, the consequences of the state farm wildfire insurance withdrawal are immediate and significant. Many find themselves with gaps in coverage or facing sudden increases in premium costs. Some are forced to turn to the California FAIR Plan, the state’s insurer of last resort, which often provides less comprehensive protection at a higher price.

Consider the experience of Malibu and Topanga residents, who have received non-renewal notices with little warning and struggled to secure replacement coverage. Some have even been left uninsured for critical weeks or months, exposing them to devastating financial risk if a wildfire strikes.

Ultimately, the state farm wildfire insurance withdrawal signals a long-term shift in how wildfire risk is managed by the insurance industry. Traditional policies are becoming harder to obtain, and homeowners must be more proactive than ever in safeguarding their properties and demonstrating wildfire resilience.

At Matador Fire, we encourage Los Angeles homeowners to stay informed and take immediate action. Our team specializes in wildfire risk assessments, home hardening upgrades, and advanced protection strategies that can help you maintain coverage and peace of mind in this challenging new environment.

Immediate Steps for Homeowners After a State Farm Non-Renewal Notice

If you’ve received a non-renewal notice due to the state farm wildfire insurance withdrawal, you are not alone. As wildfire defense experts at Matador Fire, we have seen firsthand how these changes are affecting Los Angeles homeowners. Here’s how to take control of your insurance situation and protect your greatest asset

Step 1: Review Your Current Coverage and Policy Status

The first priority after a state farm wildfire insurance withdrawal notice is to carefully review your current policy. Read the non-renewal letter in detail to confirm your coverage end date, any grace periods, and the exact reason for non-renewal. This step is crucial because missing deadlines can leave you uninsured, creating unnecessary risk.

Check which aspects of your property are still protected until the policy expires. Identify any exclusions, such as wildfire-related damage, and take note of what will no longer be covered. Some homeowners have faced costly gaps in protection after failing to act quickly.

To avoid a lapse, act as soon as you receive your notice. For a thorough checklist of what to do next, see our emergency wildfire readiness tips. Early action gives you the best chance of securing continuous coverage and safeguarding your home.

Step 2: Research Alternative Insurance Providers

After understanding your policy status, the next step is to research other options. The state farm wildfire insurance withdrawal has left many relying on alternatives like the California FAIR Plan, surplus lines carriers, or specialty insurers. Begin gathering quotes as soon as possible, since higher demand can lead to stricter underwriting and rising premiums.

Compare policies carefully, paying close attention to wildfire exclusions and any limitations on coverage. In 2024, FAIR Plan enrollments increased by 40 percent, showing just how competitive the market has become. Shopping early gives you bargaining power and a better selection of options.

Be prepared for challenges, including higher costs and more restrictive terms. Still, persistence pays off. By being proactive, you increase your chances of finding a policy that keeps your property protected despite the state farm wildfire insurance withdrawal.

Step 3: Document and Improve Home Hardening Efforts

Strengthening your home’s wildfire defenses can make a real difference in your insurability after a state farm wildfire insurance withdrawal. Focus on home hardening measures like ember-resistant vents, fire-resistant roofing, and creating defensible space. Insurers want to know that you are reducing your property’s risk.

Document every improvement thoroughly. Take photos, keep receipts, and request inspection reports for upgrades. Some insurance providers offer discounts for certified hardening efforts, especially when you can present clear evidence of your work.

At Matador Fire, we recommend going beyond the basics. Investing in professional home hardening not only protects your family, but also positions you as a lower-risk applicant. The stronger your documentation, the better your chances of securing coverage after the state farm wildfire insurance withdrawal.

Step 4: Prepare for Inspections and Underwriting Reviews

Most insurers require an on-site inspection before issuing a policy, particularly in the wake of the state farm wildfire insurance withdrawal. Expect a thorough review of your property’s wildfire readiness, including vegetation management, building materials, and defensible space.

Common reasons for denial include overgrown landscaping, wood decks, or insufficient clearance around structures. To pass inspection, clean your gutters, trim back trees, and remove any combustible materials near your home. Preparation can make the difference between approval and denial.

If you have already invested in upgrades or professional assessments, present this documentation to the inspector. Being ready for underwriting reviews increases your odds of being approved and maintaining coverage after the state farm wildfire insurance withdrawal.

Wildfire Defense Strategies to Improve Insurability

The State Farm wildfire insurance withdrawal has left many Los Angeles homeowners reevaluating how to protect their property and maintain insurability. As wildfire risks intensify, insurers are revising their approach, making it crucial for residents to adopt proven wildfire defense strategies. From risk assessments to home hardening, these steps not only protect your home but also improve your chances of securing or retaining coverage after the state farm wildfire insurance withdrawal.

Understanding Wildfire Risk Assessments

After the state farm wildfire insurance withdrawal, understanding your property’s wildfire risk profile is the first step toward regaining coverage. Insurers evaluate factors like proximity to wildland, local topography, and building materials. These elements contribute to a risk score that directly influences eligibility and premium costs.

For example, neighborhoods in Los Angeles with higher wildfire risk scores often face stricter underwriting and elevated rates. By knowing your home’s unique vulnerabilities, you can prioritize improvements that will make the greatest impact. At Matador Fire, we provide professional risk assessments, outlining actionable recommendations that directly address the criteria insurers use post-state farm wildfire insurance withdrawal.

A comprehensive assessment prepares you for inspections and helps you communicate your property’s strengths to underwriters, setting the foundation for better insurance outcomes.

Home Hardening Upgrades That Matter Most

Not all upgrades carry equal weight when it comes to improving insurability after the state farm wildfire insurance withdrawal. Insurers favor properties that demonstrate clear mitigation steps, especially in high-risk regions.

The most effective home hardening measures include:

- Installing ember-resistant vents and fire-resistant roofing

- Replacing siding with non-combustible materials

- Upgrading to dual-pane, tempered glass windows

Consider this table summarizing upgrade ROI:

- Ember-resistant vents:

Impact on insurability: High

Typical cost: Moderate - Fire-resistant roofing:

Impact on insurability: High

Typical cost: High - Dual-pane windows:

Impact on insurability: Medium

Typical cost: Moderate - Fire-resistant siding:

Impact on insurability: High

Typical cost: High

Homeowners in Brentwood saw premium reductions and improved policy options after targeted upgrades. By focusing on high-impact changes, you can address underwriter concerns and enhance your property’s appeal in the wake of the state farm wildfire insurance withdrawal.

Creating and Maintaining Defensible Space

Defensible space is your property’s first line of defense and a critical factor for insurers since the state farm wildfire insurance withdrawal. Creating buffer zones—0 to 5 feet, 5 to 30 feet, and 30 to 100 feet from the home—can dramatically reduce wildfire risk.

Best practices include:

- Removing flammable landscaping and debris

- Spacing trees and trimming branches

- Regularly clearing gutters and roofs

Los Angeles regulations require strict compliance, and homes with well-maintained defensible space have survived even severe wildfires. For a deeper dive into these strategies, visit What is defensible space.

Taking these steps not only protects your home physically but also signals to insurers that you are a proactive, lower-risk policyholder in the context of the state farm wildfire insurance withdrawal.

The Role of Documentation and Professional Assessments

Documentation is often the deciding factor for underwriters post-state farm wildfire insurance withdrawal. Insurers want proof of mitigation, which means detailed records and professional evaluations are essential.

You should:

- Photograph all home hardening improvements

- Retain receipts and contractor certifications

- Obtain third-party wildfire readiness assessments

Some insurers now accept professional reports as evidence of risk reduction. At Matador Fire, we specialize in providing these assessments, helping you present a compelling case for coverage. Proper documentation can tip the scales in your favor and increase your odds of approval after the state farm wildfire insurance withdrawal.

Proactive defense and thorough records are your best tools for navigating the evolving insurance landscape. For personalized guidance, contact Matador Fire for a free wildfire risk consultation and let us help you regain peace of mind.

How Matador Fire Solutions Help Homeowners Protect and Insure Their Properties

The state farm wildfire insurance withdrawal has left many Los Angeles homeowners searching for ways to secure their homes and regain insurability. As wildfire defense specialists, we at Matador Fire understand the challenges you face. Our team is dedicated to providing advanced, actionable solutions to help you navigate this evolving landscape and protect your most valuable asset.

Professional Wildfire Risk Assessments and Consultations

Navigating the state farm wildfire insurance withdrawal starts with understanding your property’s unique wildfire risks. Our experts offer free, no-obligation wildfire risk assessments for Los Angeles homeowners. We analyze your home’s vulnerabilities, considering factors like building materials, landscaping, and proximity to wildland areas.

After our assessment, you receive a custom report detailing specific weaknesses and actionable recommendations. This documentation is invaluable when applying for new coverage or appealing non-renewals resulting from the state farm wildfire insurance withdrawal. By identifying risks early, you can prioritize upgrades and present a stronger case to insurers.

Ember-Resistant Upgrades and Home Hardening Services

Home hardening is critical in the wake of the state farm wildfire insurance withdrawal. Insurers are now scrutinizing the resilience of building materials and construction features. At Matador Fire, we install certified ember-resistant vents, fire-resistant roofing, and other durable materials proven to withstand wildfire conditions.

Our team documents every upgrade with photos and receipts, helping homeowners demonstrate their commitment to wildfire mitigation. For example, after our upgrades, a Calabasas homeowner improved their insurability despite the state farm wildfire insurance withdrawal. These improvements not only increase safety but also align with insurer requirements.

Professional-Grade Fire Retardant Application

One highly effective strategy against the state farm wildfire insurance withdrawal is the use of professional-grade fire retardants. We apply eco-friendly, non-toxic fire retardants to homes and surrounding landscapes. This extra layer of protection is trusted by agencies like Cal Fire and the US Forest Service.

During the 2023 wildfires, properties treated with our solutions remained protected, even as neighboring homes faced significant threats. Our application process is safe for families and pets, and it provides peace of mind amidst the uncertainties caused by the state farm wildfire insurance withdrawal.

On-Demand Wildfire Defense Systems

Facing the state farm wildfire insurance withdrawal, many homeowners are seeking proactive defense options. Our on-demand wildfire defense systems are custom-designed for your property. These systems empower you to create a protective barrier before evacuation, reducing the risk of ember intrusion and structure loss.

We integrate advanced technology to ensure reliability and ease of use. Homeowners interested in how these innovations work can learn more by visiting our Wildfire protection technology explained page. Our solutions are designed to meet evolving insurer expectations and provide a unique advantage in high-risk areas.

Community-Wide Wildfire Resilience Initiatives

The state farm wildfire insurance withdrawal has impacted not just individuals but entire neighborhoods. Matador Fire partners with HOAs and neighborhood groups to deliver community-wide wildfire defense plans. We offer group risk assessments, bulk discounts on home hardening services, and educational workshops.

For example, a Beverly Hills HOA recently improved community insurability through our partnership, helping residents collectively address the challenges brought by the state farm wildfire insurance withdrawal. By working together, communities can strengthen their defenses and improve access to coverage.